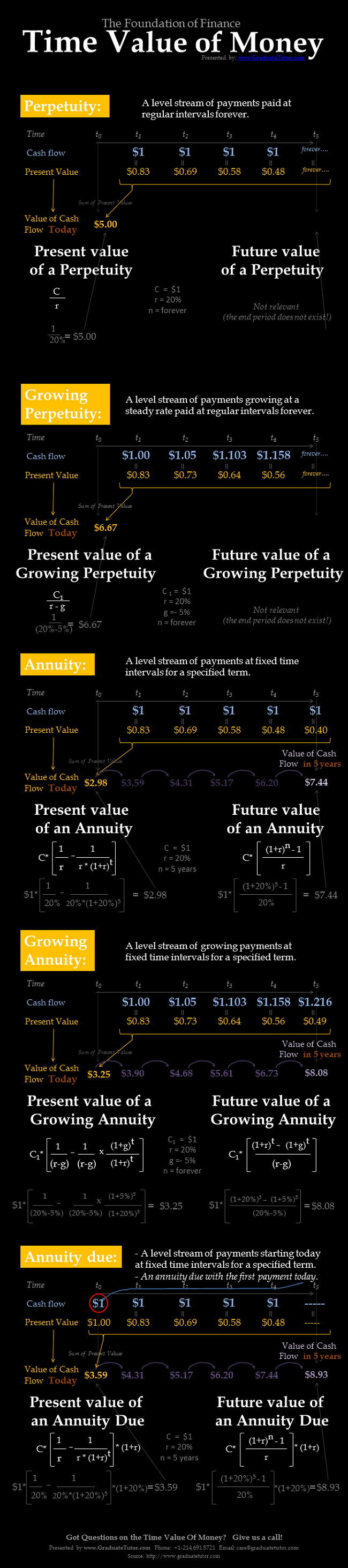

As a follow up to our Time Value of Money infographic, we have created an infographic with the most commonly used Time Value of Money formulas. The following infographic provides you the formulas for the present value of a perpetuity, present value of a growing perpetuity, present value of an annuity, present value of a growing annuity, and growing annuity. It also presents the future value of an annuity, growing annuity and an annuity due.

Feel free to use the infographic below on your website but do provide us a link.

Formulas Time Value of Money – An infographic by the team at finance tutoring team

Annuities

An annuity is a periodic stream of equally-sized payments for a specified duration. The word annuity is derived from the Latin word annum (yearly). Any stream of periodic payments of equal size can be treated as an annuity. An example of an annuity is a mortgage payment. Mortgage payments are made monthly, are of equal size, and is paid for a fixed period of time. So a mortgage loan is an example of an annuity.

The two types of annuities are:

- Ordinary annuity

- Annuity due

What are Ordinary Annuities

An ordinary annuity is an annuity in which the first payment takes place at the end of the first period. In other words, the first payment is made one period from today. Most annuities are ordinary; some examples are:

- Coupons paid by a bond

- Car loan payments

- Mortgage payments

- Student loan payments

- Social security payments

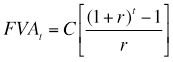

The Future Value of an Ordinary Annuity

The future value of an ordinary annuity is the sum of money you will have at the end of the annuity period. The formula for computing the future value of an ordinary annuity is:

where:

- FVAt = future value of a t-period annuity

- C = the periodic cash flow

- r = periodic interest rate

- t = number of periods until the sum is received

As an example, suppose that a sum of $1,000 is invested each year for four years, starting next year, at an annual rate of interest of 3%. Since the cash flows start next year, this is an ordinary annuity. What is its future value? In this case, t = 4, r = 3% and C = $1,000. Using the formula above, we will arrive at the future value of this annuity as follows.

FV=1000*((((1+3%)^4)-1)/3%) = $4,183.63

Alternatively, the future value of each individual cash flow can be computed and then combined as follows:

The first cash flow is invested for three years (from year one to year four):

FV3 = PV*(1+r)^t

FV3 = 1,000*(1+.03)^3

FV3 = 1,000*(1.09273)

FV3 = $1,092.73

The second cash flow is invested for two years (from year two to year four):

FV2 = PV*(1+r)^t

FV2 = 1,000*(1+.03)^2

FV2 = 1,000*(1.06090)

FV2 = $1,060.90

The third cash flow is invested for one year (from year three to year four):

FV1 = PV*(1+r)^t

FV1 = 1,000*(1+.03)^1

FV1 = 1,000*(1.03)

FV1 = $1,030.00

The fourth and final cash flow does not earn any interest since it is not deposited into the bank until year four. The future value is therefore $1,000.

The sum of these future values is:

$1,092.73 + $1,060.90 + $1,030.00 + $1,000.00 = $4,183.63

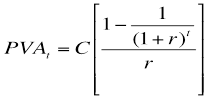

The Present Value of an Ordinary Annuity

The present value of an ordinary annuity is the value, today, of the annuity stream you will receive over the life of the annuity. The formula for computing the present value of an ordinary annuity is:

where:

- PVAt = present value of a t-period ordinary annuity

- C = the value of the periodic cash flow

- r = periodic interest rate

- t = number of periods until the sum is received

As an example, how much must be invested today in a bank account that pays 5% interest per year in order to generate a stream of payments of $1,000 in each of the following three years? In this case, t = 3, r = 5% and C = $1,000. Using the formula above, we will arrive at the present value of this annuity as follows.

PV = 1000*((1-(1/((1+5%)^3)))/5%) = $2,723.25

Alternatively, the present value of each individual cash flow can be computed and then combined as follows:

The present value of the first cash flow (paid in one year) is:

PV = FVt / (1+r)t

PV = 1,000 / (1+.05)1

PV = 1,000 / 1.05

PV = $952.38

The present value of the second cash flow (paid in two years) is:

PV = FVt / (1+r)t

PV = 1,000 / (1+.05)2

PV = 1,000 / 1.10250

PV = $907.03

The present value of the third cash flow (paid in three years) is:

PV = FVt / (1+r)t

PV = 1,000 / (1+.05)3

PV = 1,000 / 1.15763

PV = $863.84

The sum of these present values is:

$952.38 + $907.03 + $863.84 = $2,723.25

Annuity Due vs Ordinary Annuity

In an annuity due, the first payment occurs at the end of the first period. With an annuity due, the first payment takes place now or immediately. This is a less common type of annuity than the ordinary annuity. An example of this would be a lease agreement or a loan where the first payment is due immediately.

Due to the timing of the cash flows, the present value and future value of an annuity will be affected by whether the annuity is an ordinary annuity or an annuity due.

The Future Value of an Annuity Due

The future value of an annuity due is computed as follows:

FVAdue = FVA ordinary * (1+r)

This shows that the future value of an annuity due is greater than the future value of an ordinary annuity. The difference is the return of one time period as a result of the first payment made one time period ahead of the ordinary annuity. This is because each cash flow of an annuity due is invested for one additional year.

Referring to the previous example, the future value of an annuity due would be: 4,183.63(1+.03) = $4,309.14

This can be confirmed by computing the future value of each cash flow individually. Each cash flow will be invested for one additional year compared with the ordinary annuity.

The first cash flow is invested for four years (from today to year four):

FV4 = PV(1+r)t

FV4 = 1,000(1+.03)4

FV4 = 1,000(1.12551)

FV4 = $1,125.51

The second cash flow is invested for three years (from year one to year four):

FV3 = PV(1+r)t

FV3 = 1,000(1+.03)3

FV3 = 1,000(1.09273)

FV3 = $1,092.73

The third cash flow is invested for two years (from year two to year four):

FV2 = PV(1+r)t

FV2 = 1,000(1+.03)2

FV2 = 1,000(1.06090)

FV2 = $1,060.90

The fourth cash flow is invested for one year (from year three to year four):

FV3 = PV(1+r)t

FV3 = 1,000(1+.03)1

FV3 = 1,000(1.03)

FV3 = $1,030.00

The sum of these future values is:

$1,125.51 + $1,092.73 + $1,060.90 + $1,030.00 = $4,309.14

The Present Value of an Annuity Due

The present value of an annuity due is computed as follows:

PVA due = PVA ordinary * (1+r)

This shows that the present value of an annuity due is greater than the present value of an ordinary annuity. This is because each cash flow of an annuity due is paid one year sooner, so that the invested principal earns less interest. As a result, a larger sum must be invested in order to generate the appropriate cash flows.

Referring to the previous example, the present value of an annuity due would be: 2,723.25(1+.05) = $2,859.41

Alternatively, the present value of each individual cash flow can be computed and then combined as follows:

The first cash flow is withdrawn immediately, so the present value equals $1,000.

The present value of the second cash flow (paid in one year) is:

PV = FVt / (1+r)t

PV = 1,000 / (1+.05)1

PV = 1,000 / 1.05

PV = $952.38

The present value of the third cash flow (paid in two years) is:

PV = FVt / (1+r)t

PV = 1,000 / (1+.05)2

PV = 1,000 / 1.10250

PV = $907.03

The sum of these present values is:

$1,000 + $952.38 + $907.03 = $2,859.41 (Article Index)

8) Perpetuities

A perpetuity is an investment in which interest payments are made forever, but principal is not repaid. As an example, a stock that pays a regular stream of constant dividends can be thought of as a perpetuity. This is because the same cash flows are paid each year, and the stock has an infinite lifetime. Another example is a consol, which is a bond that makes interest payments forever but does not repay the principal.

The Present Value of a Perpetuity

The present value of a perpetuity that pays an annual cash flow of $C per period is:

PV = C/r

As an example, suppose that a perpetuity pays $100 per year; assume that the appropriate rate of interest is 5% per year. The present value of the perpetuity is $100/0.05 = $2,000.

The Present Value of a Growing Perpetuity

We call a perpetuity a growing perpetuity if the cash flows provided by a perpetuity grow at a fixed rate each year. The present value of a perpetuity formula is adjusted to the present value of a growing perpetuity:

PV = C/(r – g)

where:

- C = is the cashflow at the end of the first year

- r = is the discount rate

- g = annual growth rate of the perpetuity

As an example, suppose that a perpetuity currently pays $50 per year; assume that the appropriate rate of interest is 7% per year, and that the cash flow paid by the perpetuity is estimated to grow at a rate of 3% per year. The present value of the perpetuity is: $50/(0.07 – 0.03) = $1,250. (Article Index)