Investors look at a variety of valuation multiples when making investment decisions. A fundamental valuation multiple investors traditionally look at is the PE ratio which is the ‘Price-Earning’ ratio. The PE multiple is calculated by dividing the share price/earnings per share or Equity Value/Net income.

Traditionally, the PE ratio has hovered around the 10-15x range. Of course, the good companies have taken on valuations on the higher end (around 15x earnings) and mediocre companies around the lower range (around 10x earnings). Exceptional companies with high growth and good operating margins have seen PE ratios around 30x earnings. These include well-regarded companies such as Google, Apple, and Microsoft. Many analysts have been screaming overvaluation whenever they see high PE ratios!

Today, we see many companies valued at 100x earnings. Many of these companies do not even have earnings. Can we justify these valuations? When? We address these questions here.

Yes, specific factors can justify valuations that may seem crazy – even 100 x earnings.

Many investors capture these factors using the word “high growth companies”. However, these factors can be specifically listed and evaluated. A key factor is a sustainable competitive advantage, which comes from various ways, including network effects, switching costs, scale economies, channel ownership, patents, etc. Other factors that must be present include high revenue growth, good profit margins, low capital needs, and tremendous potential markets.

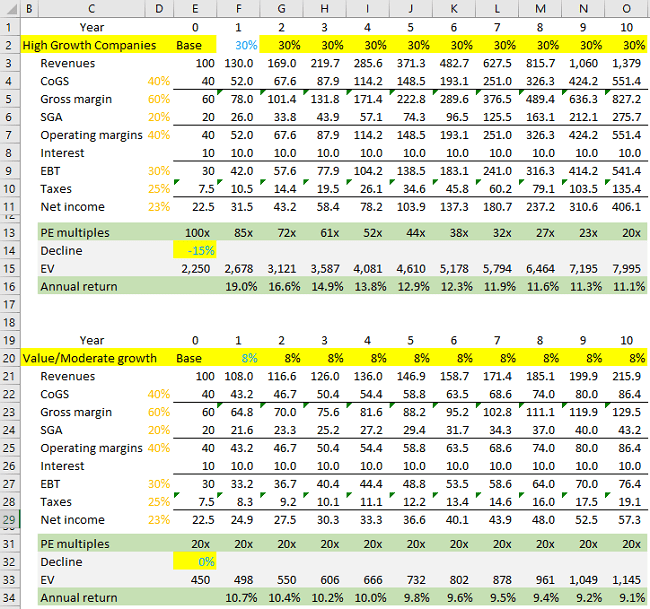

If the factors are present, a 100x or higher valuation is justified in an investment. This is true even if you expect valuation multiple contractions! See the illustration below.

.

We have compared two identical companies in the base year, assuming one is a high-growth company and the other a value company. We have assumed that the high-growth company will grow at 30%, and the value company will grow at 8%. Further, we have assumed that the high-growth company’s PE multiple will contract from 100x to 20x over ten years, and the value company’s PE ratio will stay steady at 20x. As a result, you will see that the returns on the high-growth company will exceed those of the value company, justifying the 100x earnings multiple for ‘high growth companies’ that meet the specified factors listed above.

Here is a link to the above Microsoft excel spreadsheet or view it on Google spreadsheet. Feel free to play with these figures to see the impact of different growth estimates and PE contractions on investment returns.