Financial Accounting or Introductory Accounting is usually among the first courses business school students encounter in their BBA, MBA, or CPA programs. And within Financial Accounting or Introductory Accounting, accounts receivable and associated accounts, such as allowances for uncollectable accounts or bad debt expenses, write-offs, etc., are among the topics students encounter. These topics are also important for investors and analysts studying the financial health of companies. So our accounting tutors get a lot of requests on these topics.

Therefore, we discuss the following questions related to accounts receivable and associated accounts in this article:

Investor / Application Related Questions on Accounts Receivable & Related Transactions

- Why are Accounts Receivables important to understand?

- What can I learn about a business by studying Accounts Receivables, Allowances & Write-offs?

- What is the Connection between Accounts Receivables and Cookie Jars?

- Accounts Receivable Turnover Ratio

Basic Concepts of Accounts Receivables, Allowances & Write-offs

- What are Accounts Receivables?

- What are Bad Debt Expenses?

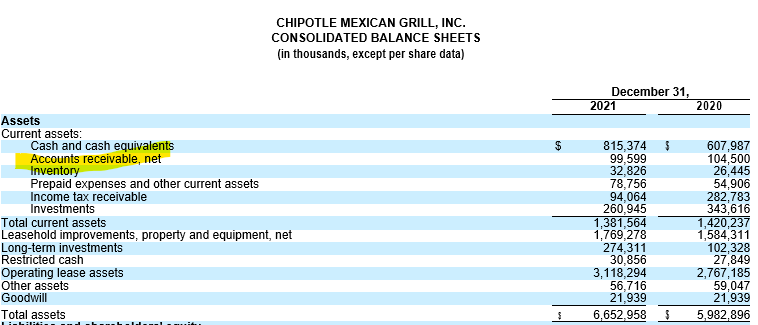

- Where do you see Accounts Receivables related Items in a Balance Sheet?

- Where do you see Accounts Receivables related Items in the Income Statement?

- Where do you see Accounts Receivables related Items in a Cashflow Statement?

- What is the difference between Accounts Receivables vs. Accounts Receivables, Net?

- Why do we need Allowances for Doubtful Debts?

- What is the Principle of Conservatism in Accounting? How does this relate to Accounting for Accounts Receivables?

- What are the Different Methods of Computing the Provision for Doubtful Debt?

- How is a Write-off Different from an Allowance for Doubtful Debt?

- How is Bad Debt Expense different from an Allowance for Doubtful Debt?

Journal Entries to record Accounts Receivable & Related Transactions

- What are the Journal Entries used to Record Bad Debt Expenses?

- What are the Journal Entries used to Write-off Accounts Receivable?

- What are the Journal Entries used to Record Cash Collection from a Previously Write-off of Accounts Receivable Account?

Accounts Receivable Bootcamp: Spot Trouble Ahead!

Accounts receivables may be a good leading indicator of financial troubles or fraud. Attend a 1-hour boot camp where you learn to investigate the Accounts Receivables of companies you invest in.

Feb 18, 2023 10 am Eastern time

Emails us at care@graduatetutor.com with any questions or clarifications.

Why are Accounts Receivables Important to Understand?

Accounts receivable and related accounts help you understand the operating characteristics of a business. Changes in these accounts can also be an early indicator of financial trouble in a company.

The management of a firm is allowed to make judgments about the provisions or allowances for bad debt expenses and uncollectable accounts. Management often uses this ability to make judgments to hide material information from investors. Therefore studying changes in accounts receivable and related accounts help you get a better understanding of what is happening inside a company. The management must be able to provide sound reasons for any noticed patterns or trends or changes in these accounts.

What can I learn about a business by studying Accounts Receivables, Allowances & Write-offs?

You can learn a lot about a business by studying the company’s accounts receivables and related accounts. Studying the allowances for uncollectible debt, provisions for bad debt expense, write-offs, related notes to the financial statements and footnotes, etc., can tell you much more about the company than management statements (especially if it is unpleasant news). For example:

- How quickly can the firm collect its receivables? Has it been stable, taking more or less time?

- How good have the estimates or provisions for bad debts been? Realistic, conservative or aggressive?

- Has there been a change in the company’s strategy or tactics?

- Has there been a change in the customer mix?

- Has the firm been increasing revenues by selling to less credit-worthy customers?

- Is the firm trying to manipulate earnings in either direction? Boost earnings or depress earnings?

What is the Connection between Accounts Receivables and Cookie Jars?

Cookie jar accounting or cookie jar reserves are terms given to an accounting practice where a company keeps profits hidden in a good time period to use in the future when it may perform poorly. A cookie is considered a treat to a boring meal. Similarly, cookie jar accounting or cookie jar reserves allow a company to pull out a treat for investors during a poor quarter or year.

The provision for bad debt expenses is one way a company can remove profits in one period and keep them aside for another accounting period when it has done poorly. This can also be done to time profits for a large bonus payout or prepare for a sale of the company, etc.

Accounts Receivable Turnover Ratio

The accounts receivable turnover ratio is a ratio used to analyze the business’s operating characteristics. The formula for the accounts receivable turnover ratio is:

Accounts Receivables Turnover = Net Annual Credit Sales ÷ Average Accounts Receivables

If we do not have the break up of credit sales, we can also use the sales figure instead:

Accounts Receivables Turnover = Net Annual Sales ÷ Average Accounts Receivables

The accounts receivable turnover ratio gives us insight into how efficiently the firm is able to collect its receivables. Firms with higher bargaining power tend to be able to collect receivables faster. Therefore a higher turnover is usually better. But this may not always be the case, as more credit usually leads to more sales. So the accounts receivable turnover must be referenced to historical trends of this firm and other firms in the industry.

The “Investigating Firm health with Accounts Receivables” workshop is on Feb 17, 2023. Email us if you are interested in knowing more.

What are Accounts Receivables?

Companies choose to sell to customers for an immediate cash payment or ‘on credit.’ When a company chooses to offer credit to customers, they allow customers to pay for the goods or services in a specific period of time, say ten days, 60 days, or 180 days, etc. Credit sales are also referred to as ‘on account.’ Each sale has an accounting entry or journal entry, and each customer has an accounts receivable account that shows the money owed to the company by that customer.

Accounts receivables is a balance sheet line that records the total amounts a company’s customers owe them as of the date of the balance sheet. It sums up all the individual accounts receivable accounts that show the money owed to the company by individual customers.

Note that there are other receivables that are not accounts receivables: For example, notes receivables are usually debt, or non-trade receivables are receivables that are not part of the regular business.

What are Bad Debt Expenses?

Unfortunately, not all the customers who owe the company money will pay the company. Some customers will default. So the company, following the principle of conservatism required by the account regulations, must account for these defaulters. This company cannot show the total accounts receivables as an asset in its balance sheet but only the amounts it expects to collect from its creditors. Companies, therefore, set aside some portion of their sales as uncollectable and treat it as an expense of doing business. This expense is referred to as bad debt expense.

Where do you see Accounts Receivables-Related Items in a Balance Sheet?

Accounts receivable is a current asset account. So the accounts receivable account shows up in the current assets section of the balance sheet. Note that it is not the accounts receivables but NET accounts receivables that are in the balance sheet for most companies. The net accounts receivable is the allowances or provisions for bad debt and uncollectable debt subtracted from the gross accounts receivable account total.

Bad debt expense is an expense account that does not feature in the balance sheet.

Where do you see Accounts Receivables-Related Items in the Income Statement?

Bad debt expense is an income statement account that records the amount of money written off as uncollectible. Therefore, like all expense accounts, the bad debt expense or provisions for bad debt expense shows up in the income statement. Often companies show bad debt expenses as a deduction to revenues. This is similar to sales returns, sales discounts, refunds, etc. However, others treat it like another expense and is considered a cost of sales. If the provision for bad debt expense is not material to be shown as a separate line item, it is rolled up as part of the selling cost in the expenses section.

Accounts receivable is a current asset account, and the allowance or provision for bad debt/uncollectable debt is a contract asset account. So these two accounts do not feature in the income statement.

Where do you see Accounts Receivables-Related Items in a Cashflow Statement?

The statement of cash flows shows how changes in balance sheet accounts and income affect cash and cash equivalents. It shows the impact of cash flows on operating, investing, and financing activities. Since accounts receivables are part of the normal operating cycle of the business, you will see accounts receivable-related items in the operating section of the cash flow statement. There are two parts that should be visible.

First, the bad debt expense is added back to the net income to arrive at the cash flow from operating activities. This is because bad debt expense is a non-cash item. The bad debt expense is only a provision for future bad debts, and it does not impact cash flows directly.

Second, changes in accounts receivables are added or subtracted from the net income to show changes in cashflows from operating activities to make it reflect cash movements in and out of the firm because sales are accounted for using the accrual concept.

What is the difference between Accounts Receivables vs. Accounts Receivables, Net?

Accounts receivables and NET accounts receivables are two types of financial accounts used to account for a company’s accounts receivable in a company’s book of accounts. The difference between them is that accounts receivables represent the total amount of money owed to a company by its customers, while accounts receivables, net, takes into account any allowances for bad debt or provisions for bad debt and subtracts it from the total accounts receivables balance.

In other words, the accounts receivables account reflects the gross amount of receivables while the accounts receivables, net, reflects the net amount after subtracting allowances for bad debt or provisions for bad debt.

Why do we need an Allowance for Doubtful Debt?

Unfortunately, not all the customers who owe the company money will pay the company. Some customers will default. So to reflect a more realistic picture of the accounts receivable, we need to reduce the value of the accounts receivable to the amount we expect to collect.

We do this by accepting that there will be some defaults and consider some defaults an expense of doing business. We call this expense bad debt expenses. Since we do not know which customers will default, we set aside some of the receivables as an allowance for defaults (like a medical emergency fund). We call this allowance an allowance for uncollectable debt. This allowance or (fund) is used to write off accounts receivables in the future when a default happens.

Why don’t we just wait for a default and then write off the receivable then? We recognize the revenues in the year of sale according to the accrual concept. So we also need to recognize the related costs, including the cost of defaults this year, according to the matching principle in accounting. This is why we cannot wait to know the default values to acknowledge the default and write off the receivable.

What is the Principle of Conservatism in Accounting? How does this Relate to Accounting for Accounting Receivables?

In accounting, the principle of conservatism, also known as the “prudence” principle, requires that accountants use caution when estimating the value of assets and liabilities.

This means that when there is uncertainty about the value of an asset or revenues, accountants should use the lower possible values. However, when there is uncertainty about the value of a liability or an expense, accountants should use the higher possible values.

Assets or revenues =====> Reflect LOWER value

Liabilities or an expense =====> Reflect HIGHER value

The principle of conservatism is intended to ensure that a company’s financial statements do not overstate its assets or understate its liabilities. This principle is used to ensure that the financial statements are conservative, are not optimistic, and do not overstate the financial health of the company.

However, if there is a bias in the financial statement, it is a bias towards a lower value of the company, which is why it is called the “principle of conservatism.” However, to achieve accounting neutrality which is the absence of bias from financial estimates, the FASB removed the principle of conservatism from its conceptual framework in 2010 and emphasises neutrality more.

The principle of conservatism applies to accounting for receivables because it requires the company to be very careful in reporting the value of accounts receivables. When valuing accounts receivables, the company accept that not all receivables will be collected and account for the loss from uncollectible accounts.

Different Methods of Computing the Provision for Doubtful Debt?

There are several methods for computing the provision for doubtful debt, including:

- Percentage of receivables: The percentage of receivables method involves estimating the percentage of accounts receivable that are likely to default or be uncollectible. This estimate is usually based on historical figures of uncollectable receivables or defaults. Once an estimate has been arrived at, the company can take the same percentage of receivables as the value of receivables that will not be collected and provide for the corresponding provisions.

- Aging of receivables: The aging of receivables method categorizes the accounts receivables by various age categories. For example, accounts receivables are categorized into less than 30 days old, less than 90 days old, etc. We estimate the amount of default expected for each category based on historical figures.

- Individual assessment: The individual assessment method involves looking at each accounts receivable account individually and deciding the likelihood of default. The individual assessment method is appropriate when each account is large, and there are only a limited number of accounts. It is also used when specific factors apply to certain accounts, such as bankruptcy or industry turmoil in a segment of customers, etc.

- Percentage of credit sales: The percentage of credit sales method assumes that a percentage of all credit sales will go bad. This estimate is based on prior experience from credit sales. For example, if the company’s historical bad debt rate is 3% and credit sales for the period are $1,000,000 then the bad debt expense would be 3% * $1,000,000 = $30,000.

The aging of receivables method and the percentage of credit sales method are the most commonly used methods. The aging of receivables method maybe the more accurate, but the percentage of credit sales method is simpler to implement.

How is a Write Off different from an Allowance for Doubtful Debt?

A write-off and an allowance for doubtful debt are two different parts of accounting for uncollectible accounts.

An allowance for doubtful debt is an estimate made by a company of the value of accounts receivable that will not be collected. This estimate is used to reduce the value of accounts receivable on the balance sheet, making the financial statements more realistic or conservative. The allowance for doubtful debt is an estimate, and it is a contra account to accounts receivable on the balance sheet. An allowance for doubtful debt does not cancel the debt obligation of any specific debtor. This is the case even if we use the specific identification method or individual assessment method. We only provide for a chance that some debtors may default.

A write-off, on the other hand, is the actual removal of an account receivable from the balance sheet when it is determined to be uncollectible. A write-off is a specific identification of an account receivable that is bad. We then cancel or zero out that receivable identified as a default. We are essentially using the provision for bad debt or the allowance for doubtful debt kept aside earlier for these write offs. After the write-off, the customer account is considered closed, and the company may not make any further attempts to collect the debt.

In summary, an allowance for doubtful debt is an estimate of bad debts, whereas a write-off is the actual removal of an account receivable when it is determined to be uncollectible.

How is Bad Debt Expense Different from an Allowance for Doubtful Debt?

Bad debt expense and an allowance for doubtful debt are related, but they are not the same thing.

An allowance for doubtful debt is an estimate made by a company of the value of accounts receivable that may not be collected. This estimate is used to reduce the value of accounts receivable on the balance sheet, making the financial statements more realistic or conservative. The allowance for doubtful debt is an estimate at a point in time and is a contra account to accounts receivable on the balance sheet. The allowance for doubtful debt or uncollectibles is a cumulative account and is not reflected in the income statement.

Bad debt expense, on the other hand, is a provision or setting aside some expense for a likely loss incurred by a company from defaults or uncollectible accounts. It is considered an expense and recognized as an expense in the income statement, reducing the company’s net income. There are various ways used to compute the bad debt expense. This is an annual expense and not a cumulative account.

In summary, an allowance for doubtful debt is an estimate of bad debts, and it is used to adjust the value of accounts receivable on the balance sheet. Bad debt expense, on the other hand, is a provision or setting aside some expense for a likely loss incurred by a company from defaults or uncollectible accounts. It is considered an expense and recognized as an expense in the income statement, reducing the company’s net income.

What are the Journal Entries used to Record Bad Debt Expenses?

Bad debts are treated as an expense and hit the income statement reducing the profits and retained earnings of the firm. Therefore we debit the bad debt expense account to increase bad debt expense. Bad debt expense is also referred to as a provision for bad debts.

The other side of the transaction is the allowance for doubtful debts. The allowance for doubtful debts account is also referred to as an allowance for uncollectable accounts. This is a contra account that is set off against the accounts receivable account in the balance sheet. Therefore, we credit the allowance for doubtful debts account to increase it.

Dr. Bad Debt Expense ————–$500

Cr. Allowance for Doubtful Debts ————–$500

Please remember that the provision for doubtful debts is made in the same accounting period as the sales occur. This is true even if we know do not know who will default in this current period.

What are the Journal Entries used to Write-off Accounts Receivable?

When we become aware that a particular customer will default, we must acknowledge that we will not receive his dues. So we need to write off his balance from the accounts receivables account. Since it reduces the accounts receivable, we credit the accounts receivable account.

Because we have already provided for this loss as an expense at the time of sale, we do not need to record an additional expense. Therefore the other side of the transaction hits the allowance for doubtful debts account. We are reducing the money left to cover doubtful accounts. This is a contra account that is set off against the accounts receivable account in the balance sheet. Therefore, we debit the allowance for doubtful debts account to decrease it.

Dr. Allowance for Doubtful Debts —–$300

Cr. Accounts Receivable ————–$300

What are the Journal Entries used to Record Cash Collection from a Previously Write-off of Accounts Receivable Account?

Sometimes, an account receivable account that was written off surprises and pays fully or partly the amounts due. An example can of a bankruptcy proceeding that was able to repay creditors all or part of their dues. In these situations, we first reverse the write-off journal entries we did at the time of the write-off to activate the receivable.

Dr. Accounts Receivable ————–$300

Cr. Allowance for Doubtful Debts ———$300

We then record the collection of cash to close the accounts receivable account.

Dr. Cash ——————————–$300

Cr. Accounts Receivable ————–$300

If we can assist you with understanding accounts receivables, allowances for uncollectables, provisions for bad debts, or write-offs of accounts receivables, please feel free to email or call us. Or join the Accounts Receivable Boot Camp.

Note to self: Writeoff Formula, Case Matching Examples